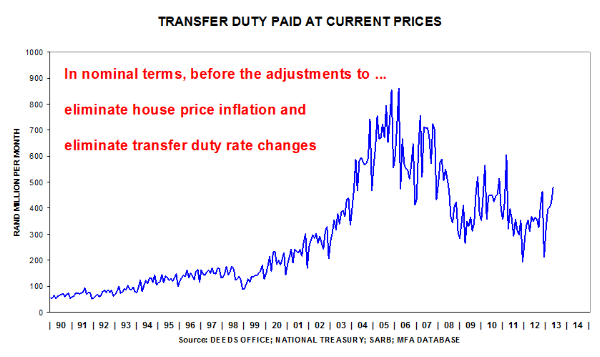

Transfer Duty Paid

Transfer duty is payable when existing dwellings are purchased (on new houses, VAT is payable). Therefore, the cyclical movement in this particular tax can be regarded as a good proxy for the well-being of the residential property market.

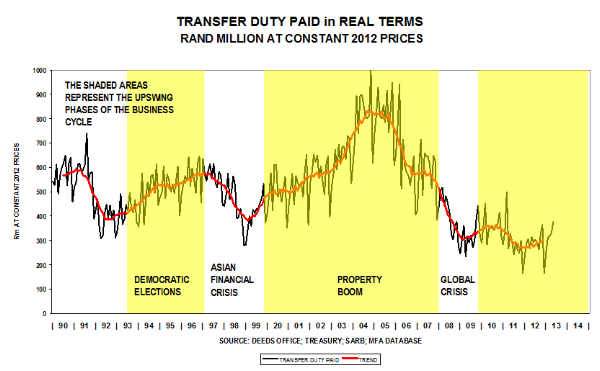

To determine real trends, one needs to adjust the nominal values for house price inflation and for changes to the rate of transfer duty payable. At the moment the threshold for the payment of transfer duty relates to houses that change hands for more than R600 000. This threshold is meant to make it more affordable for middle class people to own their own home.

The three accompanying graphs, reflecting data up to May 2013 and show the following:

- That, in nominal terms, the level of the indicator has recovered from the December 2011 slump.

- That, in real terms (stripping inflation out and adjusting for transfer duty rate changes), a sharp rise in the level of transfer duty is evident.

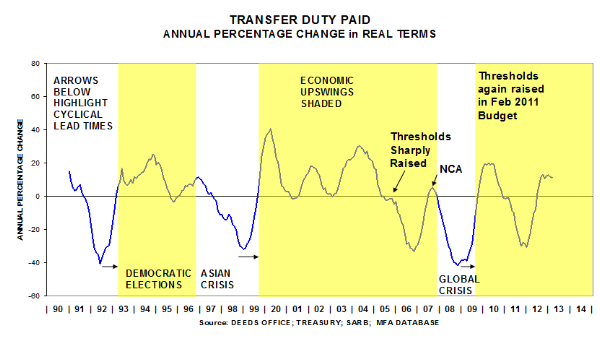

- That the real smoothed annual percentage change is currently 11.3%. This finding represents a dramatic improvement because the annual decline in January 2012 was -31.3%.

Due to the drop in mortgage rates during July 2012, it is quite likely that this indicator could improve further in coming months, reflecting better business conditions in the residential property market. We expect this revival to be modest because of the still high debt levels of consumers and low growth in mortgage lending figures.

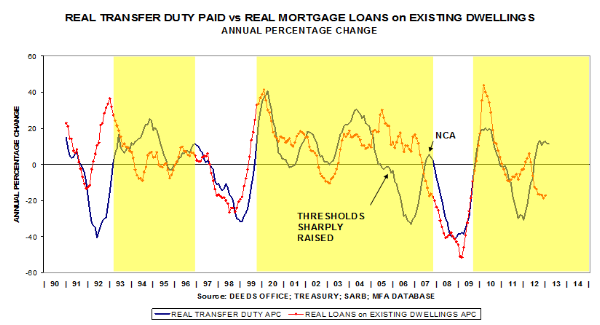

One can assume that most existing dwellings are financed with mortgage bonds.Because both indicators are related to the residential property market, one could reasonably expect that movements in mortgages advanced for dwellings could be closely linked to movements in transfer duty paid.

It makes sense to compare these two indicators that function as proxies for the well-being of the residential property market. Observe in the next graph that the cyclical movements, expressed as annual percentage changes, are remarkably close.

Where the correspondence is not that close, the divergence can be explained by means of changes to transfer duty rates or increases in threshold levels (e.g. 2005, resulting in a loss to the Fiscus).One can also observe the dramatic drop in these key indicators during the global financial crisis of 2008/09. During this period the residential property market suffered severely.

Recent trends are positive and it looks like national market conditions are improving. There is clear evidence that the market has finally turned. Observe that the Transfer Duty Paid indicator is in positive territory, but that the movement in Loans Granted has turned negative.

There is a publication lag of three months, with Loans Granted being the lagging indicator. Weak loans data in July-Sep 2012 could explain this divergence. The latest data to March 2013 suggest that Loans granted could be turning the corner.